Title loans in Missouri are a common option for those who are dealing with a financial emergency. However, you must have a smart title loan repayment plan to reduce additional stress and ensure you can get the money back to the lender. Remember, failing to repay a title loan can result in you losing your car, so you need to have a plan in place before borrowing.

In this guide from Missouri Title Loans, Inc., we will explain how to budget after a title loan. This title loan repayment plan within 30 days in Missouri can help you budget the cost of repayment to ensure you can afford to pay back the loan, with interest, to avoid car repossession and late fees.

Smart Title Loan Repayment: A 30-Day Budget Plan For Borrowers

Title loans are fast, efficient loans that let you borrow money based on your vehicle's value. They are simple loans to get approved for, as you just need these three required items: a driver’s license, a lien-free vehicle title in your name, and a vehicle for inspection. You can also get approved in person in 30 minutes and access fast cash within one business day.

What’s a little less fast and simple is title loan repayment. Many borrowers, who are struggling financially already, may not know how to fit title loan repayment into their budget. Thankfully, we have some tips and a plan you can try to afford title loan repayment.

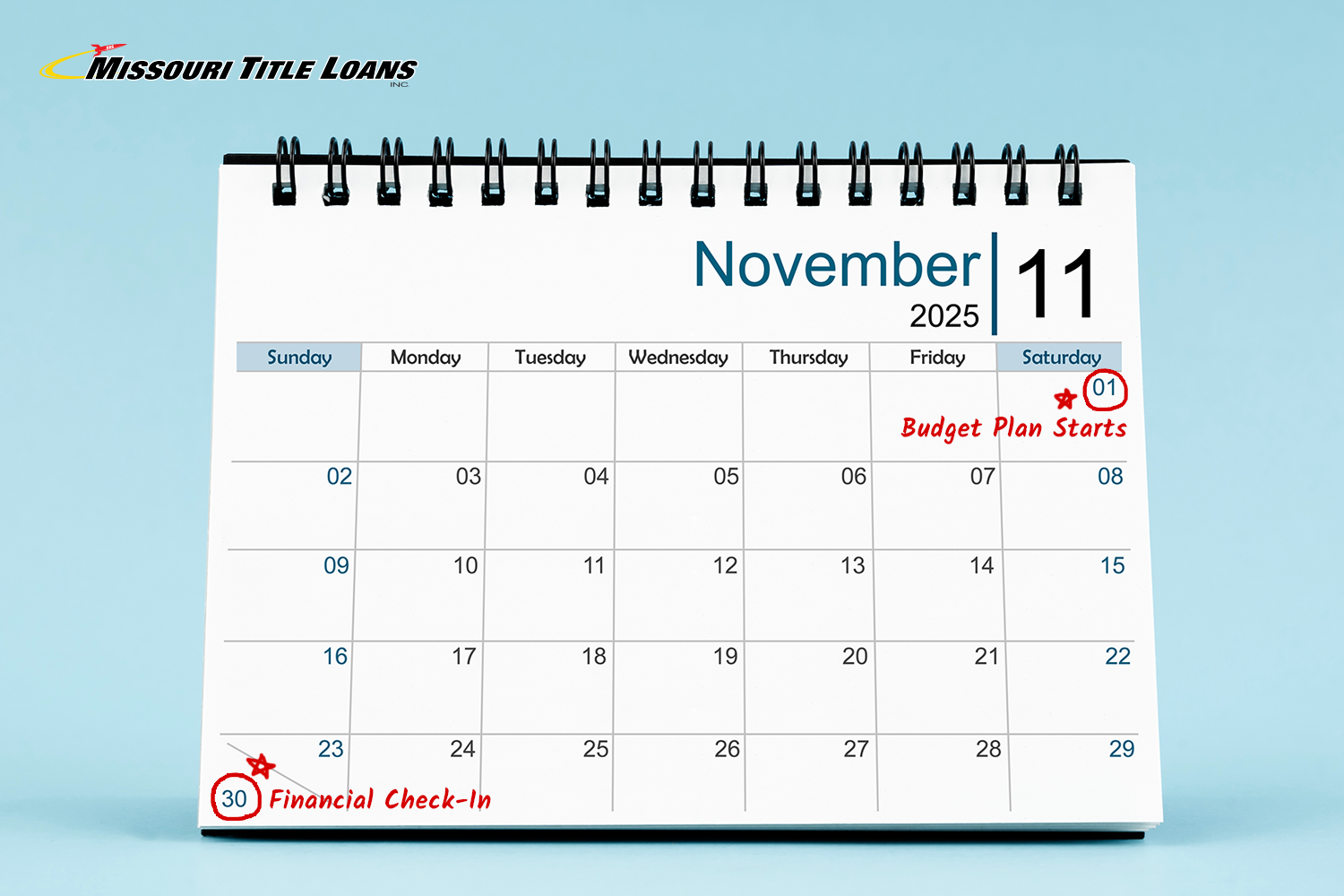

Here is a 30-day plan for how to budget after a title loan:

Week 1: Assess Your Finances

The week you get your title loan in Missouri, you need to start thinking about how to pay it back. It is essential that you don’t wait until the last moment. A lot of people make this mistake, which can lead to financial struggles and a potential debt trap. During the first week, you should consider your financial position to begin building your repayment plan.

In week one, assess your finances by listing out the following:

- Income – Make a list of all the money you have coming in. Note when you receive the cash, and how much. Don’t just think about employment income. Think about any benefits you may be receiving, too. It doesn’t matter how small the income source is; put it on your list.

- Expenses – Make a note of all your outgoings. This includes larger obligations such as rent, mortgages, and loans. You should also think about phone bills, internet, and any streaming or subscription services. Food should also be considered. Don’t forget to consider your title loan repayment here. At this point, you might notice some non-essential costs you can cut.

- Priorities – You’ll now want to separate your expenses into lists. Consider the most urgent repayments, e.g., rent, food, and your title loan. These are the ones where you need to pay for, or you could run into issues. Non-essential bills may include streaming services or outgoings that could be delayed for a short while.

Doing this will accomplish a couple of things. Firstly, you’ll know whether you’ve got enough cash rolling in to cover all your expenses. If you haven’t, then you’ll know which expenses to cut while you prioritize repayment. Now that you have a holistic view of your financial situation, you can begin building your repayment plan.

Week 2: Make A Repayment Strategy

In the second week, you’ll want to start drawing up a list of when money will be coming into your account and when repayments on loans need to be made.

Ideally, you’ll want to be paying off loans as quickly as you can. A lot of people wait until the end of the month to pay off any debts. If you wait, you’re far more likely to run out of money. You are also far more likely to miss payments, which can lead to extra fees and negative marks on your credit report.

Set aside the money you need for essentials and start paying off your loans. You should be funneling all of your leftover money into title loan repayment. Remember, these loans collect interest, so the faster you can pay them off, the better. If you can afford to pay off your title loan now, do so. If you still think you are going to struggle with title loan repayment, it’s time to start cutting costs.

Week 3: Cut Costs And Boost Cash Flow

While trying to pay off your title loan in 30 days, you might find that finances are a little bit tighter than normal. You should take the opportunity to cut costs wherever possible. In fact, this shouldn’t just apply to the month your title loan is due; you should be thinking about how to budget after a title loan and beyond.

Here are some of the ways to cut costs and afford car title loan repayment:

- Eating out or getting food delivered

- Buying coffee instead of making it at home

- Unnecessary subscription services

- Luxury items (jewelry, video games, Blu-rays, etc.)

- Non-essential food (candy, cookies, chips, etc.)

- Expensive night outs (bars, concerts, etc.)

If cash is really tight, you’ll need some extra money flowing in. In the short term, this means selling any unwanted items on online marketplaces. In the long term, you might want to consider a part-time job or perhaps freelance work. You can use websites like Fiverr or Upwork to get freelance gigs as a writer, editor, graphic designer, and much more.

Week 4: Plan For The Future

By week 4, hopefully, you will have met all your financial obligations, and the future will look a bit brighter. Wrap up any last money you need to repay. Your work isn’t done yet, though. You’ll need to start planning for the future to avoid a situation like this in the future.

You have two goals this week:

- Set aside emergency funds – Anything you don’t spend this month can be put away for a rainy day. It doesn’t matter if it is only a few dollars. A few dollars each month will quickly add up. Your goal should be to save 3-6 months’ worth of expenses in case you face a financial emergency or lose your job.

- Build a budget for the next month – With your title loan paid off, you should have more cash available. Don’t budget to spend it all. Try to stick as close as you can to the budget you built in week 1. This will give you extra funds in case of a financial emergency, reducing the chance you’ll need a future title loan.

Borrow Responsibly With Missouri Title Loans, Inc.

At Missouri Title Loans Inc., we understand that sometimes you need to turn to alternative funding sources. They aren't a long-term fix for financial problems, but they can serve as a quick solution for essential expenses that help you get your budget back on track. Use it responsibly for necessary costs and make smart title loan payments, and you could potentially create a brighter financial future.

Many people use title loans to lower fees on unexpected bills or to help cover expenses while waiting for their paycheck. Others may use their title loan to pay for unforeseen costs like auto repairs, medical bills, and travel expenses. No matter how you use your title loan funds, always borrow responsibly. Never borrow more than you need or can repay.

Getting a title loan from Missouri Title Loans, Inc. is a quick process. In many cases, you could receive funds the same day or by the next business day at the latest. This means you can inquire about a title loan whenever you need one. You can qualify even with poor credit, as long as you own your car outright. Apply online and get approved at one of our Missouri locations within 30 minutes.

Get Your Finances Back On Track With A Title Loan In Missouri

With proper budgeting and trimming of non-essential expenses, it shouldn’t be too difficult to pay back a title loan within 30 days. Title loans can be useful when you have unexpected expenses you cannot afford before your next paycheck. You can borrow up to $15,000 today, and you won’t have to worry about your credit score!

Are you facing a financial emergency? Get the financial help you need with Missouri Title Loans, Inc.; fill out our online title loan form today. You can then visit us in person to qualify within 30 minutes.

Note: The content provided in this article is only for informational purposes, and you should contact your financial advisor about your specific financial situation.